Electronic payment is a subset of an e –commerce transaction to include electronic payment for buying and selling goods or services offered through the internet. Generally we think of electronic payment are referring to online transactions on the internet, there are actually many forms of electronic payments.

As technology is developing, the range of devices and processes to transact electronically continues to increase while the percentage of cash and cheques transactions continues to decrease.

So in other word an electronic payment system is needed for compensation for information of goods and services provided through the internet such as access to copyrighted materials, database searches or consumption of system resources-or as a convenient form of payment for external goods and services-such as merchandise and services provided outside the internet. It helps to automate sales activities, extends the potential number of customer and may reduce the amount of paper work.

Cashless economy is a situation in which the flow of cash within an economy is non-existent and all transactions are done through electronic media channels such as direct debit, credit and debit cards and electronic clearing and payment systems such as Immediate Payment Service (IMPS), National Electronic Funds Transfer (NEFT) and Real Time Gross Settlement (RTGS).

Today, credit cards and online payment services are becoming increasingly popular in urban India, paper currency notes are still an essential part of daily life. One saying is revenue is vanity, cash flow is sanity but cash is king. Cash may be defined as any legal medium of exchange that is immediately negotiable and free of restrictions.

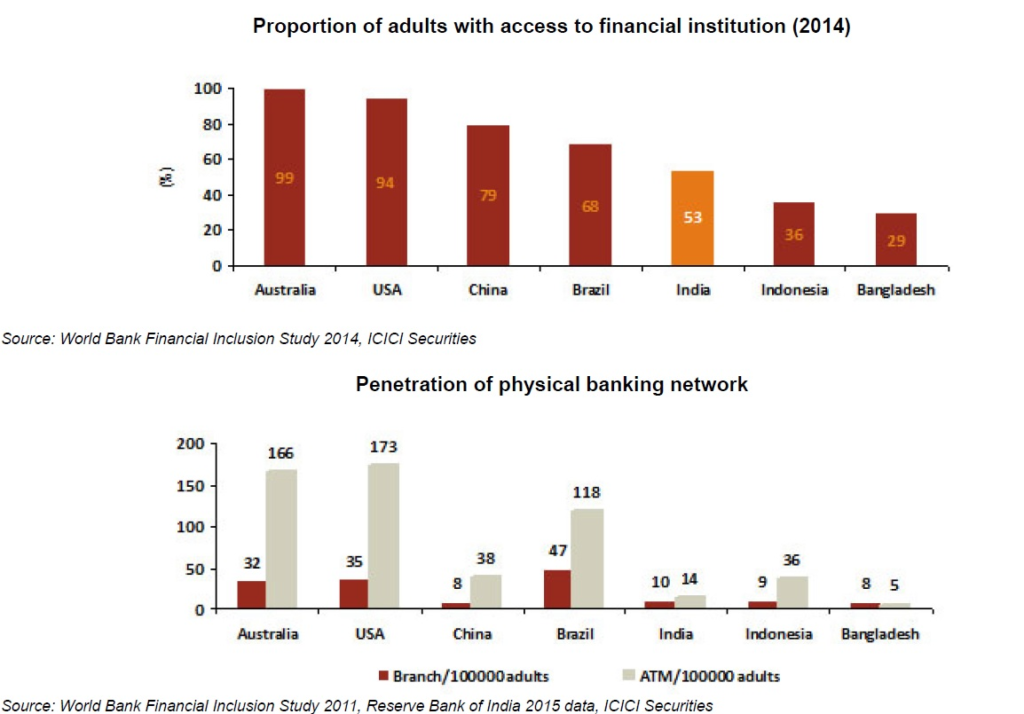

We are the fourth-largest user of cash in the world. The rate of cash to GDP is the highest, i.e. 12.42% in India. Cash in circulation to private consumption ratio in India is 20% and Card transactions account for 4% of the personal consumption expenditure. As most of people are illiterate, poor, engaged in small transactions and having less banking habits.

For people cash is the most convenient, preferred and easy form of medium of exchange, hassles free. A cash transaction is immediate and doesn’t involve any intermediary. Cash provides individuals and families with liquidity. Once needs not to worry about a computer system crashing, power going off, and losing transaction midway.

Use of cash doesn’t involve any extra cost as in the use of debit/credit cards. Even in the most cashless countries like France and the Netherlands, cash still accounts for 40% or more of all consumer transactions.

Usually cashless economies have low corruptions and less black money. Almost every country is bracing towards cashless economy and many countries have made significant progress. It is just a world trend which India is trying to catch up.

- Global Market

Historically, payments have been viewed as utility products, fundamentally transactional and tactical in nature, undifferentiated and volume-driven. A payment was often perceived as the final step in a transaction, with limited opportunity to provide value-added services or solutions.

However, this competitive market is getting redefined by the advent of non-traditional payment providers, evolution of new solutions, changing customer expectations and changing global demographics. A shift in global trade flows and the currency market’s role remains crucial in formulating invention and adoption of differentiated payment services.

A vast geographical and demographic stretch lies beyond the formal payment system in emerging countries. This unbanked and under banked market has a huge revenue generation potential for financial institutions. According to reports produced by Accenture and CARE International, UK, financial institutions can garner $380 billion in additional revenue through financial inclusion, thereby tapping the untapped pie. It is estimated that nearly $270 billion in additional revenue can be generated through small businesses whereas inclusion of unbanked adults into the formal financial system could generate another $110 billion.

India, being a financially fragmented market, offers huge potential in terms of revenue generation avenues. The country has an unbanked population of nearly 23.3 crore in 2015 though it has improved from 55.7 crore in 2011 (according to a report by PwC). Rapid development of new payment concepts and business structures is expected to displace cash and other traditional forms of payments.

Launch of the Pradhan Mantri Jan Dhan Yojana (PMJDY) has fuelled the inclusion of a higher proportion of the population into the formal financial system. PMJDY has added 19.3 crore accounts with Rs 26,940 crore deposits mobilised as of November 18, 2015 though a large proportion of these accounts (~36%) are zero balance accounts. Emergence and rapid growth in ecommerce (India’s e-commerce business has increased to $14 billion in 2015) is instrumental in inducing a shift towards digitised payment.

A sustained fall in Smartphone cost and development of telecom infrastructure (over half a billion Indians are expected to switch to Smartphone’s in the next five or six years) coupled with rapidly growing internet-connected population is expected to keep the e-commerce momentum buzzing. It is anticipated to touch ~$100 billion by 2020 (Nasscom).

- The Story so far

The payments industry has been experiencing advancement, growth and innovation at a steady rate. Demonetization was a learning curve which gave a push to the payments market. It urged and compelled customers to look beyond traditional cash transactions.

Digital payments started to pick up pace with the growth of e-commerce companies followed by emergence of digital wallet companies. The consumers, the digital wallets provide attractive offers and cash backs to get consumers on board using the payment channel. Thanks to the ease of use, attractive offers and increased Smartphone penetration, the digital wallet companies did find their way to the consumer’s phone as well as the pocket.

To expand their reach, the digital wallets started encouraging customers to use them for offline point of sale (POS) transactions too like at shopping malls, supermarkets, grocery stores, restaurants and gas/petrol stations. These POS transactions are expected to become a majority contributor to the digital payments platform in the coming years. Clearly, digital wallets are playing a unique role in driving the growth of digital payments sector.

The other important pillar of the digital payment story are the online ticketing, travel and events companies like IRCTC (Railways), Makemytrip, Yatra, Ibibo, Cleartrip (Airlines and hotels), Trivago (hotels), redBus (buses), and Bookmyshow (movie and event ticketing). They have got consumers to transact online.

- The Potential

The digital payment industry is gaining momentum and is projected to grow at an exponential rate. 81 per cent of existing digital payment users prefers the medium over other non-cash payment methods like cheques or demand drafts. Online shopping, payment of utility bills (like electricity, mobile bills, water bills, etc.) and movie tickets are the three things that an Indian user primarily pays for through digital platform.

An interesting angle to India’s digital payment story is that it is going to be dominated by micro transactions (tractions of value lower than Rs 100). In fact, 50% of person-to-merchant transactions are to be under Rs.100 says the Google-BCG report. Alternate digital payment instruments like digital wallets, UPI, payment banks, Bharat QR are expected to grow fiercely and estimated to double their contribution to 30 per cent in the digital payment industry.

Mobile/Digital wallets: The digital payment industry growth will be led by the digital/mobile wallets. According to the Capgemini’s World Payment Report, mobile wallets will witness a compound annual growth rate (CAGR) of 148 per cent over the next five years and will be $4.4 billion by 2022. The digital wallets are also supposed to outshine UPI.

- Web and Digital Payment

Web payment contains a set of rules for the execution of payment transactions that are followed by adhering entities (payment processors, payers and payees), where transactions take place over networks (such as the Web). Some digital payment schemes make use internally of payment instruments from other payment schemes.

The Web Payments ecosystem strives to support fundamental Web principles by:

- Adhering to Web architecture fundamentals

- Supporting network and device independence

- Providing for payers and payees with differing physical and cognitive abilities

- Being machine-readable where possible to enable automation and engagement of nonhuman entities

- Protecting the privacy of all participants

In addition to the fundamental Web principles above, the Web Payments ecosystem also

strives to:

- Improve the interface experience for all stakeholders

- Provide stakeholders with unencumbered knowledge and choice when undertaking a

Payment

- Support a wide spectrum of security and privacy needs to meet industry expectations

- Support existing payment schemes while enabling new ones

- Encourage efficient settlement

- Facilitate compliance with legal and regulatory obligations

- Enable monetization on the spectrum of Web to native apps

Web payment contains a set of rules for the execution of payment transactions that are followed by adhering entities (payment processors, payers and payees), where transactions take place over networks (such as the Web). Some digital payment schemes make use internally of payment instruments from other payment schemes.

- Need for Secure Transaction

The Web payment architecture must provide the ability for participants in the payment Process to confidently, securely and accurately identify and connect to other participants that are party to the payment.

The architecture should not disclose private details of the participant’s identity or other sensitive information as part of the payment process unless required by operational, legal or jurisdictional rules, or when deliberately consented to (e.g. as part of a loyalty program) by the owner of the information.

The Web payments architecture should make this easy by standardizing the mechanisms available to issue, exchange and verify credentials as part of a payment transaction, as well as a secure mechanism for the exchange of identity information when it is explicitly required as part of a payment.

To accomplish this, it is expected that the architecture will also need to support an evolving variety of authentication and identification techniques (e.g. multifactor, biometric, etc.) which can be used independent of or in concert with a participant’s identity data.